If you plan to contract with Medicaid managed care organizations or transportation brokers in Illinois, your insurance program isn’t just a business decision — it’s a contract requirement. Get it wrong and you won’t get approved. Get it right but let it lapse, and you’ll lose your contract. This guide breaks down exactly what Illinois Medicaid MCOs and transportation brokers expect from NEMT providers when it comes to insurance.

How Medicaid NEMT Works in Illinois

Illinois delivers Medicaid NEMT services through a managed care model. The state contracts with managed care organizations, and those MCOs either manage transportation directly or subcontract it to transportation management brokers like MTM and ModivCare. As a NEMT provider, you don’t contract with the state directly — you contract with the MCO or broker, and their contract is where your insurance requirements live.

This is an important distinction because it means your insurance requirements aren’t set by a single state regulation. They’re set by the specific MCO or broker you’re contracting with, and different organizations may have different requirements. You need to read every contract carefully and make sure your insurance program satisfies each one individually.

Standard Insurance Requirements for Medicaid NEMT Providers

While specific requirements vary by MCO and broker, the following coverage types and limits represent the baseline that most Illinois Medicaid transportation contracts require.

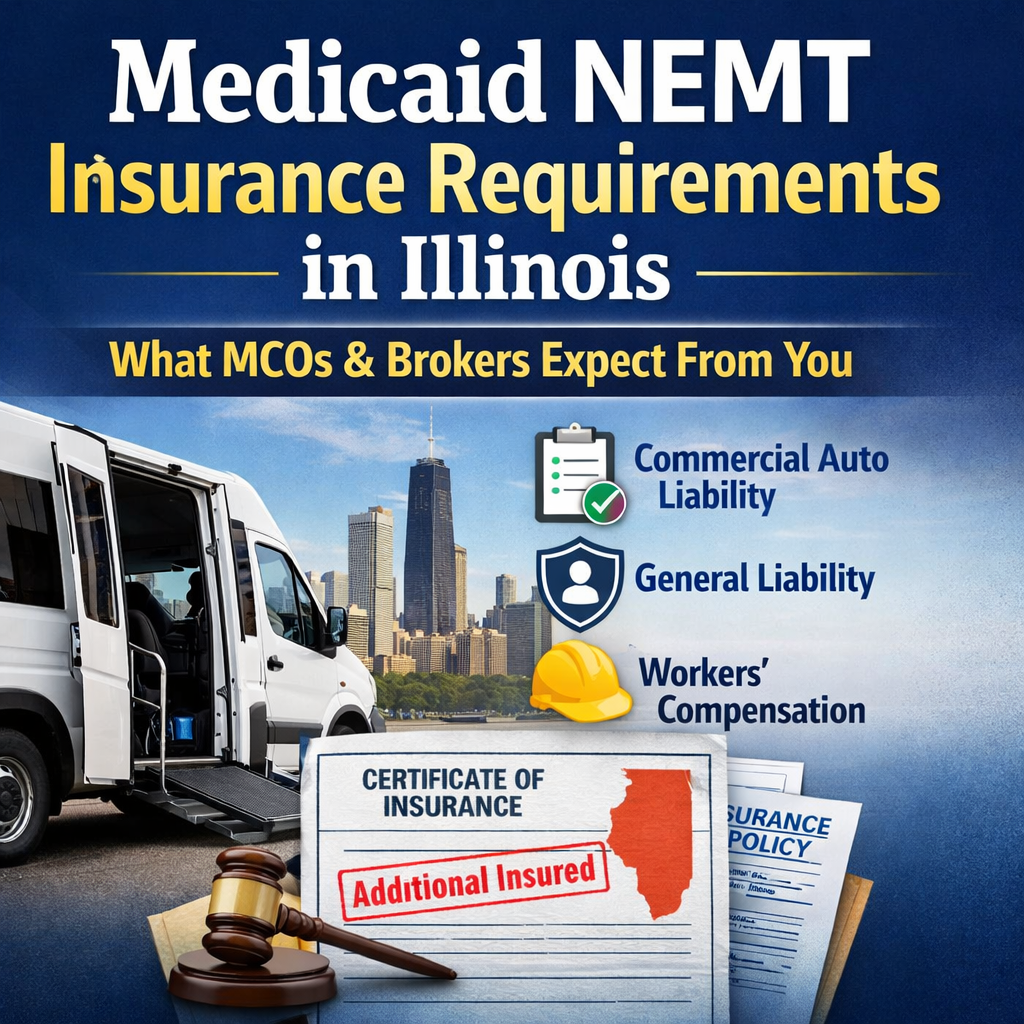

Commercial auto liability — $1,000,000 per occurrence. This is the non-negotiable minimum. Your commercial auto policy must cover all vehicles used to transport Medicaid beneficiaries and must include bodily injury and property damage liability at this limit or higher. Some MCOs require a combined single limit (CSL) of $1,000,000, while others require split limits. A few brokers are now requiring $1,500,000 per occurrence for new provider contracts.

General liability — $1,000,000 per occurrence / $2,000,000 aggregate. This covers injuries and property damage that occur outside the vehicle — during boarding, at pickup and drop-off locations, and at your business premises. Nearly every MCO and broker contract requires it.

Workers compensation — Illinois statutory limits. If you have any employees, Illinois law requires workers comp and so will your Medicaid contracts. Even if you’re a sole proprietor with no employees, some brokers still ask for a waiver on file confirming your exemption.

Hired and non-owned auto — $1,000,000. Many MCOs require this coverage even if you exclusively use company-owned vehicles. It covers the gap when employees use personal vehicles for any company purpose, and it’s increasingly a standard contractual requirement.

Commercial umbrella — $1,000,000 or higher. Not every contract requires an umbrella policy, but many of the larger MCOs and brokers do. Given the vulnerability of the passengers you’re transporting, an umbrella policy is strongly recommended even when it isn’t contractually required.

Certificates of Insurance: The Proof That Matters

Meeting the insurance requirements is only half the job. You also need to prove it. Medicaid MCOs and transportation brokers require certificates of insurance (COIs) that document your coverage types, limits, effective dates, and — critically — name the MCO or broker as an additional insured on your policies.

The additional insured requirement is where many NEMT operators run into problems. Your insurance carrier needs to endorse your policy to add each MCO or broker as an additional insured. Not all carriers will do this easily or quickly, and some charge additional fees for each endorsement. If your agent isn’t familiar with the Medicaid NEMT space, this process can cause delays that hold up your contract approval.

At Handzel & Associates, we handle COI requests and additional insured endorsements routinely for our NEMT clients. We understand the urgency — a delayed certificate can mean a delayed contract, which means delayed revenue. We make it a priority to turn these around quickly and accurately.

What Happens If Your Insurance Lapses

This is where things get serious. If your insurance coverage lapses — even for a single day — your MCO or broker is entitled to suspend or terminate your contract immediately. Most contracts include a provision requiring your insurance carrier to notify the MCO directly if your policy is cancelled or non-renewed. That notification triggers an automatic review, and if you can’t show replacement coverage immediately, you’re off the provider list.

Getting back on after a lapse is much harder than getting approved in the first place. MCOs view a coverage lapse as a serious red flag about your business practices, and some brokers have waiting periods before they’ll reconsider a provider who’s been terminated for an insurance lapse.

The takeaway: treat your insurance renewal dates with the same seriousness as your vehicle inspections and driver certifications. Set reminders 90 days before renewal to start the shopping process. Your agent should be proactively managing this for you.

Beyond the Minimums: What Smart NEMT Operators Carry

The minimum requirements get you approved for a contract. But experienced NEMT operators in Illinois typically carry coverage beyond the minimums for good reason.

Higher commercial auto limits — $1,500,000 or $2,000,000 CSL — position you to qualify for contracts with any MCO or broker without needing to adjust your policy each time. Medical payments (MedPay) coverage for passengers is not always explicitly required, but it pays passenger medical expenses regardless of fault and can prevent small injury claims from becoming lawsuits. And a higher umbrella limit — $2,000,000 or more — provides meaningful protection when a single accident involving a medically fragile passenger can generate claims well beyond primary policy limits.

The cost difference between minimum and slightly-above-minimum coverage is often surprisingly small. Talk to your agent about what it would cost to carry higher limits — the answer might change your decision. At Handzel & Associates, we regularly help NEMT operators in Illinois compare the cost of meeting bare minimums against the cost of carrying broader coverage, so they can make an informed choice.

Need help finding the right NEMT insurance? Handzel & Associates has been protecting Illinois businesses since 1989. Call (773) 725-6767 or visit handzel.com/business/nemt-insurance to get a free quote.